Will Helene Impact CRE Insurance Premiums?

As the Southeast recovers from the devastation brought by Hurricane Helene, experts are beginning to weigh its effects on insurance costs.

Hurricane Helene is not a reinsurance event, so it is unlikely to significantly impact insurance premium rates, according to Mike Chapman, national director of commercial markets for HUB International.

“This is a heavily uninsured event, so there will be big economic losses, Chapman told Commercial Property Executive, “but less so on the insured side.”

Moody’s Analytics estimates Hurricane Helene’s total property damage at between $15 billion and $26 billion, a number that could be further refined to reach an industry loss estimate.

Chapman said Helene will not be calculated into his firm’s 2024 hurricane forecast.

“We still legitimately have two weeks left, and some activity is happening in the Atlantic,” he said. “We don’t really give new predictions. We compare actual to what we projected.”

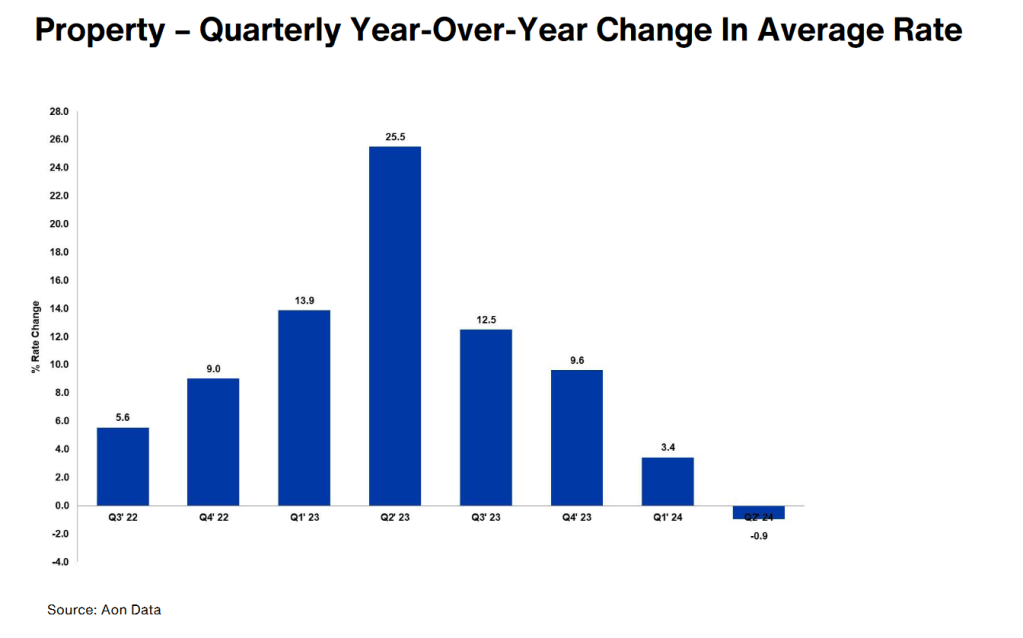

Climbing insurance rates have been far more predictable than most hurricane seasons for commercial real estate owners and operators. According to a recent report from Aon, costs rose for 27 consecutive quarters.

However, Aon’s latest property market dynamics report shows a shift. That streak ended in the second quarter of 2024, as the property year-over-year rate change decreased from +3.4 percent in the first quarter to -0.94 percent in the second quarter.

READ ALSO: Why Resilience Strategies Are a Must

Additionally, Aon’s report said that there will continue to be rate differentiation:

A -10 percent to flat rate adjustment for desirable accounts/occupancies and primarily Nat-Cat exposed accounts (excluding Florida);

Flat to 5 percent rate increases for loss-challenged or less desirable occupancies;

Flat to 10 percent or higher rate increases for Florida-only accounts or those with significant Nat-Cat exposure in Florida.

Vincent Flood, U.S. property practice leader for Aon, said the rates fell due to shifts in supply and demand.

CRE owners and operators renew their annual policies throughout the year, so the timing of the renewal date could affect their renewal rates. Aon said 70 percent of policies are renewed in the first six months of the year, with the second quarter being the busiest and the third quarter seeing the fewest renewal instances.

The streak of climbing property insurance rates ended in the second quarter of 2024, when the figure decreased to -0.94 percent. Chart courtesy of Aon

“In 2023, the insurers were profitable,” Flood said. “Reductions began in March and have accelerated since.”

The hurricane season ends Nov. 30. Flood said he’s “cautiously optimistic” that this season will be less eventful than anticipated. “But we have a long way to go,” he added. “Remember, Super Storm Sandy occurred at the end of October.”

Aon said it is too soon to assess Hurricane Helene’s impact.

Some see rate reductions

Patrick McGinley, Vestar president of management services, told CPE that prior to Hurricane Helene, the firm’s annual insurance rates had decreased by over 3 percent compared to last year.

“By maintaining high maintenance standards and adopting a proactive risk mitigation mindset, we have successfully reduced the trend of claims over the past five years, which, along with increased competition in the market, allowed for the decrease. We are committed to continuing these practices to ensure a safe and cost-effective environment in the future.”

Insurance industry confronts climate change more quickly

Ben Bailey, managing director & head of JLL’s work dynamics insurance business, said that, operationally, insurance companies are exposed to the same severe weather risks as many other financial or professional service sectors.

“The increasing severity and frequency of climate-driven events is forcing all industries to reinforce their business continuity focus and facility response plans,” he said.

According to Bailey, what makes insurance unique is the exposure companies have to claims resulting from these weather events and the corresponding premium adjustments to cover those claims. “The fact that insurance companies are being forced to confront the effects of climate change more quickly than other industries also motivates them to focus on proactively managing their own carbon emissions to avoid reputational risk,” Bailey said.

JLL has partnered with several across the industry to develop a baseline for reporting and disclosure purposes. In some instances, this helped them formulate a comprehensive portfolio strategy to achieve their carbon reduction targets.

Aon’s report also said clients could expect an aggressive underwriting approach for shared and layered accounts with desirable occupancy classes and profitable historical loss ratios, with or without heavy Nat-Cat exposures.

The post Will Helene Impact CRE Insurance Premiums? appeared first on Commercial Property Executive.

{kind=link}