ULI, PwC Release 10 Emerging Trends for 2025

Noting that the commercial real estate industry has reached “an inflection point” and things are finally looking up, the Urban Land Institute and PwC have released their Emerging Trends for Real Estate 2025 forecast for the U.S. and Canada. As usual, the annual report also identifies the top cities to watch.

The emerging trends and rising metros are based on 450 interviews and 1,600 survey results from a broad swath of commercial real estate professionals, who, the report cautioned, are still not “wildly optimistic.”

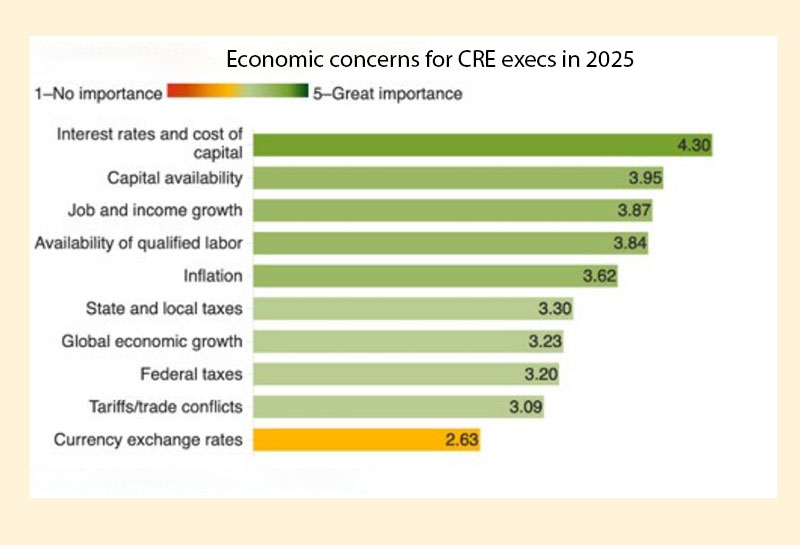

Interest rates and cost of capital are still the top economic concern for interviewees and respondents, the bulk of which are in the business of buying and selling real estate. Private property owners or commercial/multifamily developers represent 35.2 percent of the executives ULI and PwC drew their conclusions from, and real estate advisory, asset management or service companies comprise 20.1 percent. The next two greatest economic concerns were capital availability and job and income growth.

READ ALSO: What Happened to the Capital Markets

But capital costs fell slightly in importance over last year (down 40 basis points to 4.30 on a scale of 1 to 5), reflecting the Fed’s August announcement that it was ready to start dropping rates. The actual 50-basis-point cut came after most of the survey participants responded.

The three biggest social/political concerns for the respondents and interviewees for 2025 are housing followed by political extremism and immigration policy—same as last year, although immigration beat out political extremism last year.

The top concerns for developers in 2025 are construction costs, labor availability and operating costs.

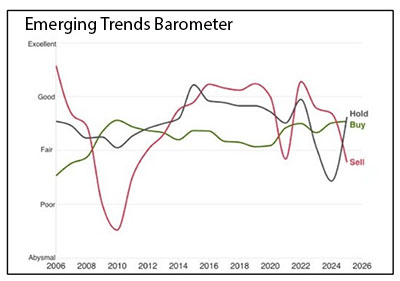

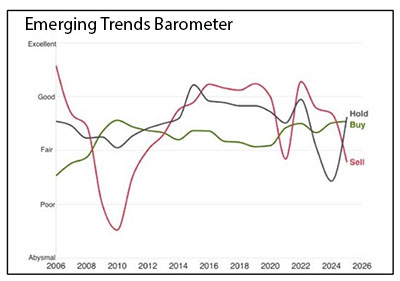

Emerging Trends for 2025

1. Be Careful What You Wish For

The Fed has begun making long-awaited interest rate cuts and respondents expect increased economic certainty to boost transaction volume and even some development. But CRE executives are also wary of how slower economic and job growth (i.e., the Fed’s soft landing) could impact demand, NOI and price appreciation. In sum, there is “a mixed outlook” for commercial real estate.

2. New Cycle Begins

“Healing” in the capital markets is beginning to enable the price discovery that has eluded the market since the Fed began hiking interest rates in March of 2022. There is ample capital—at a slightly more reasonable price—for acquisitions and refinancing. As investors reduce their “exposure,” they will be more willing to take on “new exposure.” On the equity side, there is a growing consensus that prices have troughed.

3. Building Boom, Tenant Boon

Demand for most property types is stronger than pre-pandemic levels, respondents reported. In office, however, there is a “painful reckoning” of a seemingly more permanent nature. Oversupply in a number of property types has created a true tenant’s market. However, the report finds a widening bifurcation between newly constructed prime office and industrial spaces and older spaces with fewer amenities. Tenants’ advantage will be lessened once the development pipeline slows down. In multifamily, oversupply has led to falling rents, particularly in the Sun Belt. But demand is expected to absorb supply.

4. Now Where?

The report finds that Sun Belt migration has moderated as the region’s cost advantage is evaporating in many locations and relocation costs (moving expenses and higher interest rates) increase. Climate change will be a bigger factor in moves in coming years, and could also contribute to a slowing of Sun Belt migration since many of the catastrophic weather events occur in that region.

5. Many Solutions, No Answers

While most new housing production tends to be market-rate or luxury due to high construction costs, there is a sense that housing of any type is welcome and that lower-income residents will be able to occupy units vacated by the residents who move to newer buildings in a process called “filtering.” A federal solution to the housing crisis is needed, and both presidential candidates are promising to address the problem during their prospective administrations.

Source: Emerging Trends in Real Estate 2025 Survey

With CRE executives getting ready for the next upcycle, the second set of trends is property-focused. Respondents rated the core property types on a scale of 1 to 5, with industrial ranking highest and office ranking lowest for investment. Single-family housing ranked highest and office ranked lowest for development.

Key trends for property types

1. Industrial Smart Growth

Industrial tenants will be carefully curating their logistics portfolios, focusing on supply chain efficiency, network diversification, technology and sustainability. Savvy owners and developers will be tailoring their product to cater to tenants’ more refined appetite for space. Nearshoring and onshoring will drive manufacturing growth.

2. Data Centers: Navigating Power Constraints and Skyrocketing Demand

The data center business is exploding, and CRE investors are clamoring to satisfy demand. “Development is highly profitable compared to other forms of real estate and long leases with credit tenants support high loan-to-value ratios,” the report authors wrote. Tenants’ intense power requirements currently make development challenging, but that is preventing the market from getting oversupplied and keeping rents high, the report found.

3. Senior Housing: Building New Muscle

As capital for new senior housing becomes available, the report recommends rethinking the traditional senior living models to offer more alternatives for aging baby boomers—now 20 percent of the population and growing—and for “middle-market” seniors in particular.

4. Retail Resilience: Weathering the Storm

Demand for physical retail has rebounded while there has been very little construction over the past few years, the report notes. As a result, retail vacancies are down, and rents are up. A number of retail bankruptcies and closures in 2024 seemed to threaten retail’s winning streak, but landlords have been able to backfill the space. Restaurants, experiential retail and “quasi-medical” tenants are all expanding. Drug store closures are a concern, but they also present a redevelopment opportunity.

5. Innovating the Suburbs: Is Life Sciences’ Growth

Sustainable

Life science continues to grow, though maybe not as fast as its real estate supply. According to the report, the life science inventory expanded by 20 percent since the start of COVID-19, but absorption has not kept pace in many markets. There are indications a new growth spurt for biotech is getting underway, igniting hope that new inventories will soon be absorbed.

Once again, the top 10 emerging markets for 2025 are largely focused on Sun Belt markets, though not all the same Sun Belt markets. This year, they are: Dallas/Ft. Worth, Miami, Houston, Tampa-St. Petersburg, Nashville, Tenn., Manhattan, Detroit, Columbus, Charleston and New Orleans.

In 2024, the top markets were: Nashville, Phoenix, Dallas/Fort Worth, Atlanta, Austin, San Diego, Boston, San Antonio, Raleigh/Durham, Seattle, Houston, Denver and Charlotte.

The post ULI, PwC Release 10 Emerging Trends for 2025 appeared first on Commercial Property Executive.

{kind=link}

{kind=link}