Office Report: Urban Office Distress Deepens

The wave of distress forecasted since the pandemic is now taking shape, particularly in large urban office properties facing weakened demand and expiring leases, the latest CommercialEdge report shows.

Office attendance remains low, with Kastle’s Back to Work Barometer showing average utilization stuck at 54 percent for the past two years. Vacancy rates have risen steadily, climbing 150 basis points throughout 2024 to 19.8 percent as of the end of the year. Remote work appears to be a lasting shift, further straining the sector.

In 2024, 25 million square feet of office space was involved in distressed transactions—up 39 percent from the prior three-year average of 18 million. While the overall number of deals stood right around 2,400, the share of distressed transactions jumped to 10.8 percent, with the average asset size rising by a third to over 200,000 square feet. Chicago led the nation with 26 such deals, including the 882,071-square-foot Schaumburg Towers, sold at a 15 percent discount.

With construction starts down 50 percent year-over-year, a tighter supply could offer property owners some relief as the market repositions itself.

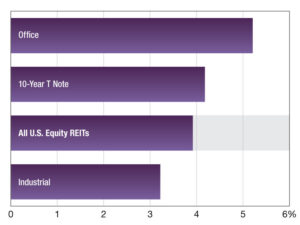

READ ALSO: What CRE Investors Want to Buy in 2025

The tech industry remains especially flexible regarding remote and hybrid work models, prompting many firms to reduce their office footprints. This trend was further compounded by a wave of layoffs that began in late 2022 and extended through 2023.

At the end of March, the national office vacancy rate reached 19.9 percent, marking a 170-basis-point rise compared to the same time last year and staying nearly flat from February. Five metros with significant concentrations of tech companies posted vacancy rates above 25 percent: Austin (28.5 percent), the Bay Area (25.5 percent), Denver (25.2 percent), San Francisco (28.6 percent) and Seattle (27.5 percent).

National full-service equivalent listing rates averaged $33.42 per square foot in March, up by one cent from February and 4.9 percent higher year-over-year. According to CommercialEdge data, Manhattan reported the highest average rate at $69.03 per square foot, trailed by San Francisco at $63.83 and Miami at $55.84.

Office-using employment expanded by 10,000 positions in March. The financial activities sector accounted for most of this growth, adding 9,000 jobs. Professional and business services gained 3,000 jobs, while the information sector contracted by 2,000 positions. Since March 2024, office-using sectors grew by 0.1 percent—the first annual increase recorded since October 2023; Slightly more than half of the markets tracked by CommercialEdge experienced year-over-year declines in office-related employment during March.

Construction pipeline contracts further

As of March, the office construction pipeline featured 45.1 million square feet, amounting to 0.7 percent of total stock, CommercialEdge shows. This slowdown in development is expected to persist; Following only 11.9 million square feet of starts in 2024, the first quarter of 2025 has seen just 2.6 million square feet in groundbreakings so far.

Boston led all metros with 6.3 million square feet of office space under construction, representing 2.4 percent of its existing inventory. Austin and San Francisco each had 3.1 million square feet underway, equal to 3.3 percent and 1.9 percent of their respective inventories. Dallas was close behind with nearly 3.1 million square feet (1.1 percent), while San Diego rounded out the top five with 2.7 million square feet (2.8 percent).

In the first quarter of the year, office property sales totaled $10.3 billion, with properties trading at an average price of $183 per square foot. Office investment was concentrated in Manhattan, which amassed $2 billion in transactions, followed by Washington, D.C. ($767 million) and the Bay Area ($727 million).

Read the full CommercialEdge office report.

The post Office Report: Urban Office Distress Deepens appeared first on Commercial Property Executive.