Mortgage Delinquency Rates Increased in Q4 2024

Commercial mortgage delinquencies increased in the fourth quarter of 2024, according to the Mortgage Bankers Association’s latest commercial delinquency report.

Commercial mortgage delinquency rates increased in the fourth quarter of 2024, with the exception of life company loans, which showed a slight decrease. Even with certain market challenges such as low occupancy rates and the uncertain impact of return-to-office mandates in the office market, and oversupply in the multifamily property market, delinquency rates remain relatively low from a historical perspective.

READ ALSO: NYU REIT Symposium Special Report: 6 Takeaways

MBA estimates that almost a trillion dollars’ worth of loans are maturing in 2025, and these maturities, coupled with more challenging economic conditions and rangebound interest rates, may result in some further increases in delinquencies if borrowers cannot successfully refinance these loans.

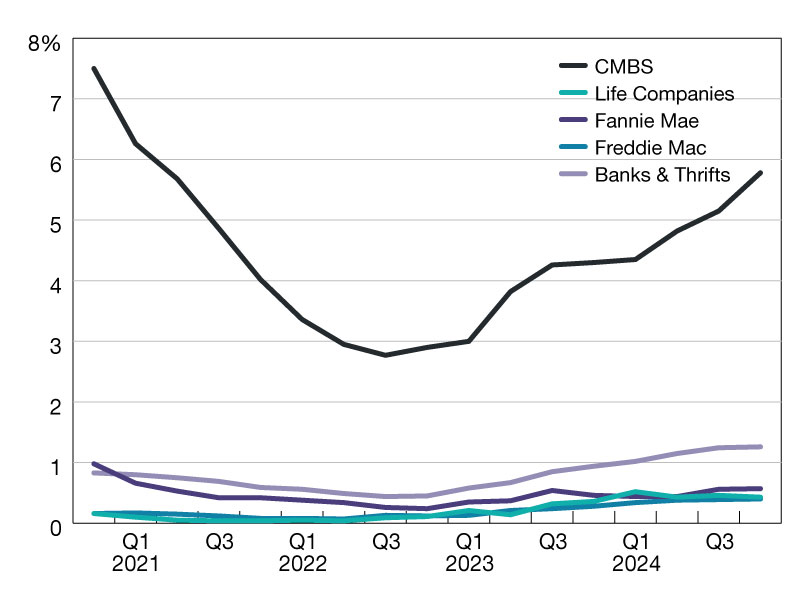

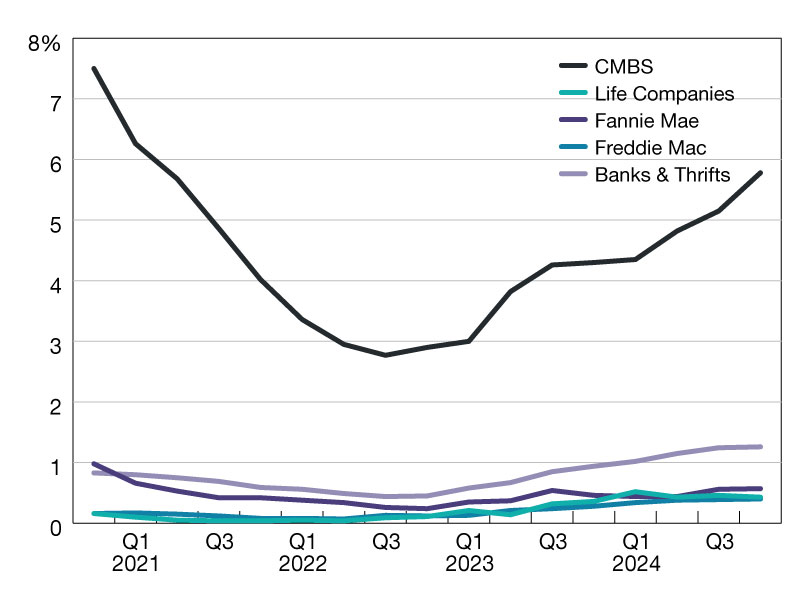

Based on the unpaid principal balance of loans, delinquency rates for each group at the end of the fourth quarter of 2024 were as follows:

- Banks and thrifts (90 or more days delinquent or in non-accrual): 1.26 percent, an increase of 0.02 percentage points from the third quarter of 2024;

- Life company portfolios (60 or more days delinquent): 0.43 percent, a decrease of 0.03 percentage points from the third quarter of 2024;

- Fannie Mae (60 or more days delinquent): 0.57 percent, an increase of 0.01 percentage points from the third quarter of 2024;

- Freddie Mac (60 or more days delinquent): 0.40 percent, an increase of 0.01 percentage points from the third quarter of 2024;

- CMBS (30 or more days delinquent or in REO): 5.78 percent, an increase of 0.63 percentage points from the third quarter of 2024.

Construction and development loans are generally not included in the numbers presented in this report but are included in many regulatory definitions of ‘commercial real estate’ despite the fact they are often backed by single-family residential development projects rather than by income-producing properties. The FDIC delinquency rates for bank and thrift held mortgages reported here do include loans backed by owner-occupied commercial properties. Differences between the delinquency measures are detailed in Appendix A.

To download the current report, visit this link.

—Posted on April 25, 2025

The post Mortgage Delinquency Rates Increased in Q4 2024 appeared first on Commercial Property Executive.