Industrial’s Uneven Playing Field

It’s a good day in industrial. In a turbulent, volatile market, the stock in trade has emerged as the biggest, safest rock in the quietest part of the harbor. Transactability in the space has been robust and is showing signs of further improvement.

However, the past two years have seen a shift in market dynamics reminiscent of George Orwell’s “Animal Farm” quote: “All animals are created equal, but some are more equal than others.” This analogy aptly describes the current industrial real estate market, where some properties spark bidding wars while others see less activity. The key to understanding this dichotomy lies in examining the market participants and their evolving strategies.

Changing of the guard

Over the past two years, core funds and open-ended diversified core equity buyers, traditionally major players in the industrial space, have largely been on the sidelines, grappling with valuation adjustments and redemption cues. In their absence, core-plus investors have stepped in, deploying their slightly more expensive capital into higher-tier assets. However, these buyers faced constraints due to investment horizons and fund life considerations.

READ ALSO: Considering a Sale-Leaseback? Get Real About Value

Properties with high credit, long-weighted average lease terms and market rents—which typically would have flown off the shelves to a hoard of bluebloods—suddenly found themselves without their usual audience. Instead, investors turned to prioritize properties that align with five-year business plans. Multi-tenant, functional Class B infill properties with immediate mark-to-market potential have fit this rubric better than anything, and the recent trades prove it. Despite the challenges of negative leverage in a higher-cost rate environment, investors were willing to tolerate this short-term disadvantage, anticipating that these deals would flip right-side up within the first 24 months.

We are now seeing renewed interest in higher credit and longer WALT opportunities, particularly where basis is the driver for the investment. As the competition in the debt markets continues to keep leverage costs low, buyer pools are deepening, and the diversity of transactions they will consider is broadening significantly.

Evolving dynamics: debt, development and demand

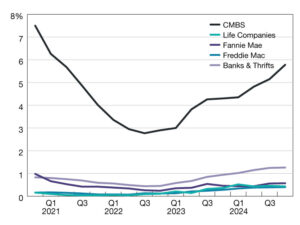

The debt market for industrial properties has also evolved considerably, offering a more diverse and sophisticated range of financing solutions. This expanded array of debt offerings is underpinning levered transactions and facilitating deal flow, partly driven by lenders’ desire to diversify their portfolios amidst some uncertainty in other sectors.

Another factor that could bolster the industrial sector’s performance is the recent slowdown in new development (down 38 percent year-over-year), which is creating a potential supply crunch, particularly in Sun Belt markets where leasing fundamentals remain strong. While some occupiers are cautious about expansion due to economic uncertainties, the underlying demand for high-quality, modern space persists.

Over the next year, leasing volumes are expected to stabilize or grow moderately as excess capacity is absorbed and delayed deals materialize. Vacancy rates may rise in the short term but should stabilize as new supply diminishes. Long-term prospects remain positive, driven by evolving supply chains, e-commerce growth and increasing demand for last-mile facilities. Additionally, the trend toward nearshoring and the need for efficient buildings are likely to support renewed rental growth, especially as construction activity normalizes from recent peak levels.

Future outlook

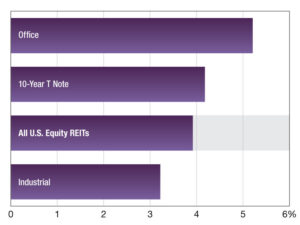

As we progress through 2025, the team on the field is rapidly changing, and several factors are converging to create a potentially favorable environment for the industrial sector. The commercial real estate market is experiencing near-record levels of dry powder, with $324 billion available for investment in 2024 and a significant portion earmarked for industrial assets. Concurrently, the ODCE funds are showing signs of re-entering the market, increasing their industrial property weightings by 18 percentage points since Q4 2019 and now accounting for 39 percent of these portfolios, which could intensify competition for prime assets.

While the broader commercial real estate market continues to face headwinds, industrial properties stand out as a relatively safe harbor, attracting investors with their potential for steady returns and long-term appreciation. However, its uneven playing field demands a new playbook. In this market of haves and have-nots, investors with an ability to act decisively will put wins on the board, while those paralyzed trying to find traction may be stuck on the sidelines.

Britton Burdette is senior managing director, JLL Capital Markets, and Bobby Norwood is managing director.

The post Industrial’s Uneven Playing Field appeared first on Commercial Property Executive.