Why Alternative Assets Are Going Mainstream

In recent months, there has been a surge of attention towards alternative assets in the real estate investment sector. One notable example is Lendlease’s $320 million sale of its U.S. military housing portfolio at, what has been described as, a “significant premium to book -value.” This sale exemplifies a trend of high-profile deals that have captured industry attention.

With a “buy-low-sell-high” strategy, Lendlease began investing in military housing in the early 2000s when it was less attractive than trophy office buildings. As the market evolved, alternative asset classes, including military housing, demonstrated superior fundamentals resulting in substantial returns for early investors.

READ ALSO: The Yin and Yang of Interest Rate Cuts

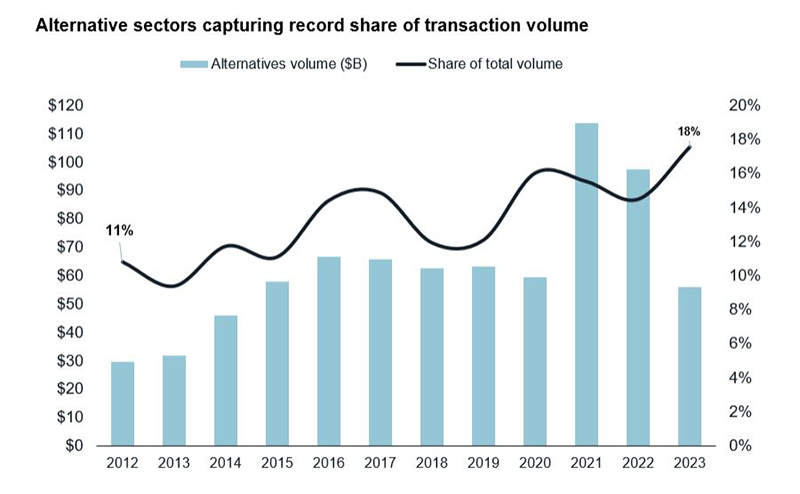

The current market landscape has been shaped by various macroeconomic factors, including technological advancements, the energy transition, housing shortages, and geopolitical challenges. As a result, alternative assets are now in high demand, with an estimated 17 percent of total U.S. commercial real estate transaction volume attributed to the sector. These non-traditional real estate opportunities are continually challenging the capital allocation norms.

Living, logistics, digital infrastructure and storage have experienced rapid growth due to increased institutional investment. Blackstone’s involvement in single-family rentals through the acquisition of Invitation Homes has mainstreamed the sector, with valuations closely aligning with traditional multi-housing properties. Blackstone remains active in SFR, recently acquiring Tricon Residential, while also investing in student housing, cold storage and data centers.

JLL’s North American Data Center report indicates a substantial increase in data center development—from 664 megawatts in H1 2020 to 5,551 megawatts in H1 2023. Major private equity firms like Blackstone, Starwood, KKR, TPG and Brookfield are active in this sector.

JLL (transactions over $5.0 million), Real Capital Analytics

While data center development remains a focus, the increasing demand for power-ready, shovel-ready sites raise questions about long-term opportunities. Smaller investors constrained by construction costs are finding opportunity in the entitlement arena. JLL Capital Markets reported over $3 billion in U.S. data center transactions in the last year, with over $1.5 billion allocated to land acquisitions spanning 1,200-plus acres. Securing the right zoning, utilities, and land use entitlements adds significant value in the competitive landscape.

Living with opportunity

The living sector is experiencing a supply shortage, leading to favorable market conditions and a record $889 billion in transaction volume between 2020 and 2023. Traditional multi-housing properties saw significant cap rate compression due to increased capital flow. However, alternative living sectors such as student housing, single-family rentals, senior housing, manufactured housing and attainable housing initially lagged in value appreciation, presenting attractive opportunities for investors.

Student housing shows strong growth potential, with undergraduate enrollment predicted to increase 9 percent to 16.8 million by 2031. Senior housing has some of the same tailwinds, as the population aged 80-plus is expected to quadruple to 21 million within the next five years. Manufactured housing is also seeing tremendous deal velocity, exemplified by Nuveen and UMH Properties’ $170 million investment in new communities last year as housing scarcity drives more people into manufactured housing.

Investors are also targeting niche sectors such as self-storage, cold storage, wind farms, solar farms and industrial outdoor parking. These asset classes show promising growth prospects in the current investment landscape, influenced by broader economic trends, consumer preferences and evolving lifestyle and work patterns.

The expansion into alternative assets benefits real estate investors by creating new opportunities and attracting fresh capital. These alternatives also serve as an outlet for capital traditionally allocated to the office sector, helping stabilize office valuations and creating accretive opportunities in both traditional and emerging sectors.

As institutional investment increases, the distinction between traditional and alternative assets blurs. The real estate investment landscape continues to broaden, with diverse investors bringing capital and liquidity to alternative sectors, potentially driving future valuation growth.

Steven Binswanger is a senior managing director with JLL. JLL is a regular contributor to Viewpoints. The firm’s most recent article can be found here.

The post Why Alternative Assets Are Going Mainstream appeared first on Commercial Property Executive.

{kind=link}